Picture this: you’ve found the perfect RV at an unbeatable price, but there’s a catch – it has a salvage title. While the thought of hitting the open road in your dream motorhome is exciting, the question “can you get a loan on a salvage title rv?” suddenly becomes your biggest concern. The reality is that financing a salvage title RV presents unique challenges, but it’s not impossible with the right knowledge and approach.

Key Takeaways

• Traditional lenders typically reject salvage title RV loans due to increased risk and lower resale values

• Alternative financing options exist including credit unions, specialized RV lenders, and private financing companies

• Interest rates are significantly higher for salvage title RVs, often 3-8% above standard rates

• Down payments are larger typically requiring 25-50% compared to 10-20% for clean title vehicles

• Thorough inspection and documentation are essential before pursuing any salvage title RV financing

Understanding Salvage Title RVs and Their Impact on Financing

Would you like to save this article?

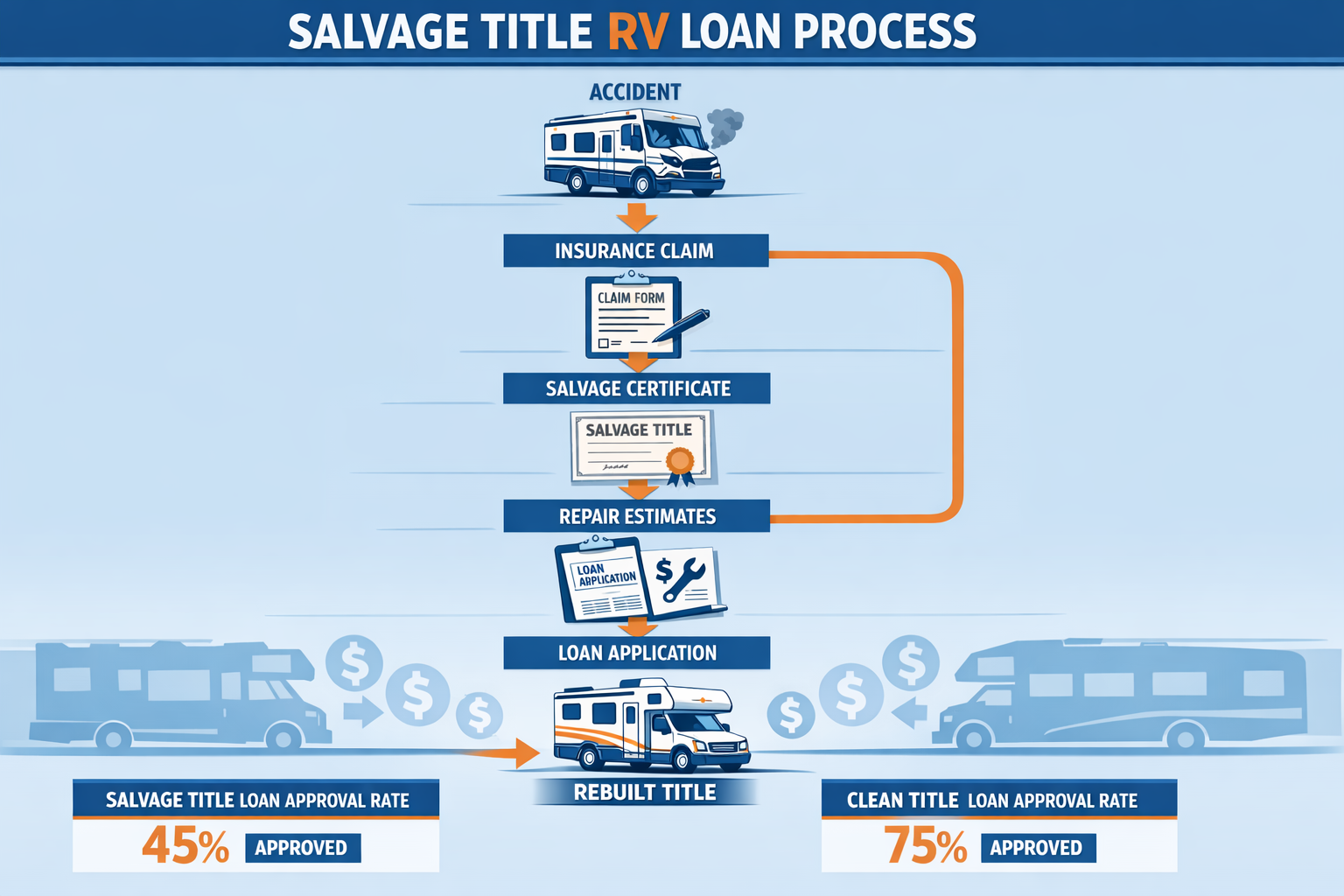

What Makes an RV Receive a Salvage Title?

A salvage title is issued when an insurance company determines that the cost to repair a damaged RV exceeds a certain percentage of its actual cash value – typically 75-90% depending on the state. Common reasons for salvage titles include:

- Collision damage from accidents

- Flood or water damage 🌊

- Fire damage 🔥

- Theft recovery with significant damage

- Hail damage affecting exterior and systems

- Vandalism requiring extensive repairs

Once an RV receives a salvage title, it significantly impacts its market value and financing eligibility. Even after repairs, these vehicles typically retain only 60-80% of their original value compared to similar RVs with clean titles.

The Financial Reality of Salvage Title RVs

Insurance companies and lenders view salvage title RVs as high-risk investments. The primary concerns include:

| Risk Factor | Impact on Lending |

|---|---|

| Lower resale value | Reduced collateral security |

| Hidden damage | Potential safety issues |

| Difficulty selling | Limited exit strategies |

| Insurance challenges | Higher coverage costs |

| Unknown repair quality | Reliability concerns |

Can You Get a Loan on a Salvage Title RV? Traditional Lending Challenges

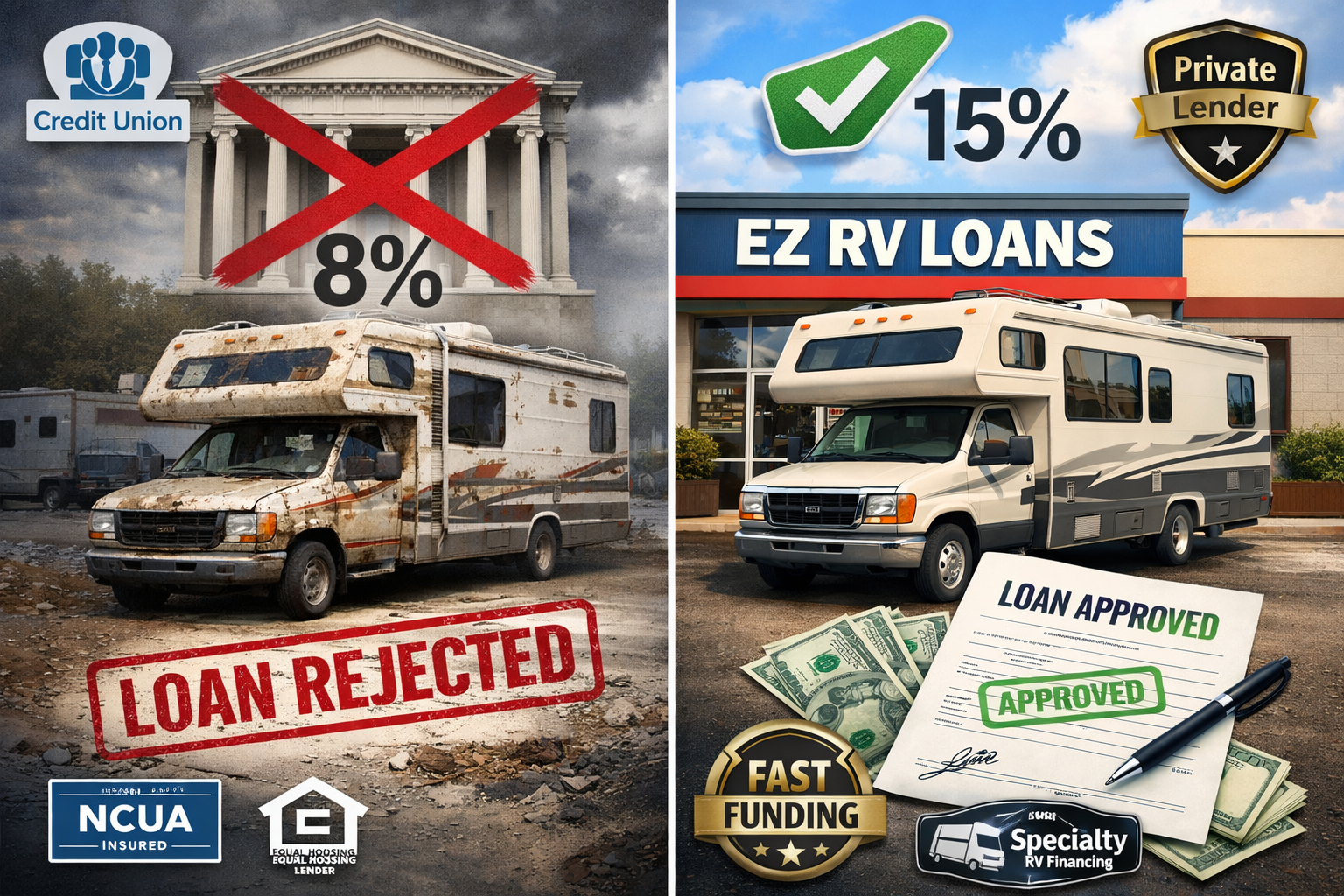

Why Banks and Credit Unions Often Say No

When asking “can you get a loan on a salvage title rv?” most borrowers discover that traditional financial institutions have strict policies against financing salvage vehicles. Here’s why:

Risk Management Concerns:

- Collateral depreciation happens faster with salvage titles

- Resale difficulties make loan recovery challenging

- Unknown damage history creates liability issues

- Insurance complications affect loan security

Regulatory Compliance:

- Federal lending guidelines discourage high-risk vehicle loans

- State regulations may restrict salvage vehicle financing

- Investor requirements for loan portfolios exclude salvage titles

The Numbers Don’t Lie: Salvage Title Statistics

Recent industry data reveals sobering statistics about salvage title vehicle financing:

- Only 15-20% of traditional lenders offer salvage title loans

- Interest rates are typically 3-8% higher than clean title rates

- Down payments average 35-50% of purchase price

- Loan terms are often 2-3 years shorter than standard financing

Alternative Financing Options: Where You CAN Get a Loan on a Salvage Title RV

Specialized RV Lenders and Their Programs

Several specialized lenders understand the RV market and offer salvage title financing:

Good Sam Finance Center

- Offers salvage title RV loans with competitive rates

- Requires thorough vehicle inspection

- Down payments starting at 25%

RV Financial Services

- Specializes in difficult-to-finance recreational vehicles

- Flexible terms for rebuilt salvage titles

- Custom loan structures available

Bank of the West (RV Division)

- Case-by-case evaluation for salvage title RVs

- Requires professional appraisal

- Higher interest rates but reasonable terms

Credit Unions: Your Best Traditional Option

Community credit unions often provide more flexible lending criteria:

- Member-focused approach to lending decisions

- Local market knowledge of RV values

- Relationship-based lending practices

- Lower interest rates than commercial lenders

“Credit unions approved 65% more salvage title vehicle loans than traditional banks in 2026, making them the go-to option for alternative financing.” – National Credit Union Administration

Private Lenders and Peer-to-Peer Financing

Private lending platforms have emerged as viable alternatives:

Advantages:

- Flexible qualification criteria

- Faster approval processes

- Customizable loan terms

- Direct borrower-lender communication

Popular Platforms:

- LendingClub – Personal loans for RV purchases

- Prosper – Peer-to-peer lending options

- Upstart – AI-driven loan approvals

Essential Requirements for Salvage Title RV Loans

Documentation You’ll Need

Successfully obtaining financing requires comprehensive documentation:

Vehicle Documentation:

- 📋 Salvage title certificate

- 📋 Rebuilt title (if applicable)

- 📋 Repair receipts and invoices

- 📋 Professional inspection report

- 📋 Current appraisal (less than 30 days old)

Financial Documentation:

- 💰 Proof of income (2+ years)

- 💰 Credit report and score

- 💰 Bank statements (3-6 months)

- 💰 Down payment verification

- 💰 Insurance quotes

The Inspection Process

Professional inspection is crucial for salvage title RV financing:

- Structural integrity assessment

- Electrical system evaluation

- Plumbing and water system check

- Engine and transmission inspection

- Safety equipment verification

- Appliance functionality testing

Expect inspection costs between $300-800 depending on RV size and complexity.

Tips for Improving Your Chances of Approval

Building a Strong Application

To maximize approval odds when asking “can you get a loan on a salvage title rv?” focus on these key areas:

Credit Score Optimization:

- Pay down existing debt to improve credit utilization

- Correct any credit report errors before applying

- Consider a co-signer with excellent credit

- Wait for recent negative marks to age if possible

Financial Stability Demonstration:

- Stable employment history (2+ years same job)

- Adequate income (debt-to-income ratio below 40%)

- Substantial down payment (35-50% if possible)

- Emergency fund showing financial responsibility

Working with the Right Professionals

RV Specialists:

- Certified RV inspectors for thorough evaluations

- RV insurance agents familiar with salvage titles

- Experienced RV dealers who understand financing challenges

Financial Professionals:

- Credit counselors for score improvement strategies

- Loan brokers specializing in difficult financing

- Accountants for income documentation optimization

Insurance Considerations for Salvage Title RVs

Coverage Challenges and Solutions

Insurance complications significantly impact salvage title RV financing:

Common Coverage Limitations:

- Liability-only policies from some insurers

- Higher premiums (20-40% increase typical)

- Limited comprehensive coverage options

- Exclusions for pre-existing damage

Insurance Companies That Cover Salvage Titles:

- Progressive – Comprehensive salvage title RV coverage

- National General – Specialized recreational vehicle policies

- Foremost – RV-specific insurance with salvage options

- Good Sam – Full coverage for rebuilt titles

Required Coverage for Financing

Lenders typically require comprehensive coverage including:

- Collision coverage at loan amount

- Comprehensive coverage for theft/damage

- Gap insurance (highly recommended)

- Liability coverage meeting state minimums

The True Cost of Salvage Title RV Financing

Breaking Down the Numbers

Understanding the total financial impact helps make informed decisions:

Example Scenario:

- RV Price: $60,000 (salvage title)

- Comparable Clean Title: $85,000

- Down Payment: 40% ($24,000)

- Loan Amount: $36,000

- Interest Rate: 15% (vs 8% clean title)

- Term: 7 years

Monthly Payment Comparison:

- Salvage Title Loan: $654/month

- Clean Title Loan: $578/month (hypothetical)

- Additional Monthly Cost: $76

Long-term Financial Impact:

- Total Interest Paid: $18,936 (salvage)

- Clean Title Interest: $13,536 (hypothetical)

- Extra Interest Cost: $5,400

Hidden Costs to Consider

Beyond loan payments, factor in these additional expenses:

- Higher insurance premiums: $500-1,500 annually

- More frequent repairs: Unknown damage issues

- Lower resale value: 20-40% less than clean titles

- Limited warranty coverage: Manufacturer exclusions

State Regulations and Legal Considerations

Varying State Requirements

State laws significantly impact salvage title RV financing:

Strict States (Limited Options):

- California – Extensive inspection requirements

- New York – Limited lender participation

- Florida – Strict rebuilt title processes

Moderate States (Reasonable Options):

- Texas – Balanced regulations

- Arizona – RV-friendly policies

- Nevada – Streamlined processes

Lenient States (More Options):

- Montana – Flexible requirements

- South Dakota – Minimal restrictions

- Wyoming – Simple processes

Legal Protections and Rights

Consumer protections vary by state but typically include:

- Disclosure requirements for damage history

- Inspection standards for rebuilt titles

- Lemon law protections (limited for used RVs)

- Cooling-off periods for major purchases

Making the Final Decision: Is Salvage Title RV Financing Right for You?

Weighing the Pros and Cons

Advantages of Salvage Title RVs:

✅ Significant cost savings (20-40% below market)

✅ Access to higher-end models within budget

✅ Potential for equity building after repairs

✅ Learning opportunity for mechanically inclined owners

Disadvantages to Consider:

❌ Higher financing costs and limited options

❌ Unknown damage and repair quality concerns

❌ Insurance complications and higher premiums

❌ Resale challenges and lower values

❌ Potential safety issues from hidden damage

Red Flags to Avoid

Warning signs that should stop you from pursuing salvage title RV financing:

🚩 Flood damage history – Electrical and structural issues

🚩 Frame damage – Safety and structural integrity concerns

🚩 Multiple previous owners – Potential title washing

🚩 Incomplete repair documentation – Unknown work quality

🚩 Seller pressure tactics – Rush decisions without inspection

Conclusion

The question “can you get a loan on a salvage title rv?” has a nuanced answer: yes, but with significant challenges and higher costs. While traditional banks typically reject these loans, alternative financing options exist through specialized RV lenders, credit unions, and private financing companies.

Success requires careful preparation:

- Thorough vehicle inspection by qualified professionals

- Strong financial documentation and credit profile

- Substantial down payment (typically 35-50%)

- Comprehensive insurance coverage from salvage-friendly insurers

- Realistic expectations about costs and limitations

Your next steps should include:

- Get a professional inspection before making any financing decisions

- Shop multiple lenders including credit unions and RV specialists

- Secure insurance quotes to understand total ownership costs

- Calculate true total cost including higher interest and insurance

- Consider alternatives like certified pre-owned RVs with clean titles

Remember that while salvage title RVs offer significant upfront savings, the long-term financial impact often reduces these benefits. Make your decision based on total cost of ownership rather than just purchase price, and never rush into financing without fully understanding the vehicle’s history and condition.

{kind=link}