Imagine scrolling through stunning RV listings online, dreaming of life on the open road, when reality hits. That beautiful motorhome costs more than many houses! 🏠 The burning question “can you get a mortgage on an RV?” suddenly becomes very real as you realize traditional home financing might not apply to your wheeled dream home.

Key Takeaways

• RV mortgages exist but differ significantly from traditional home mortgages in terms, rates, and requirements

• Financing options include specialized RV loans, personal loans, and home equity loans – each with distinct advantages and drawbacks

• Your credit score, down payment, and debt-to-income ratio play crucial roles in securing favorable RV financing

• New vs. used RVs have different financing requirements with varying loan terms and interest rates

• Understanding the total cost of RV ownership beyond the purchase price is essential for making informed financing decisions

Understanding RV Financing: Can You Get a Mortgage on an RV?

Would you like to save this article?

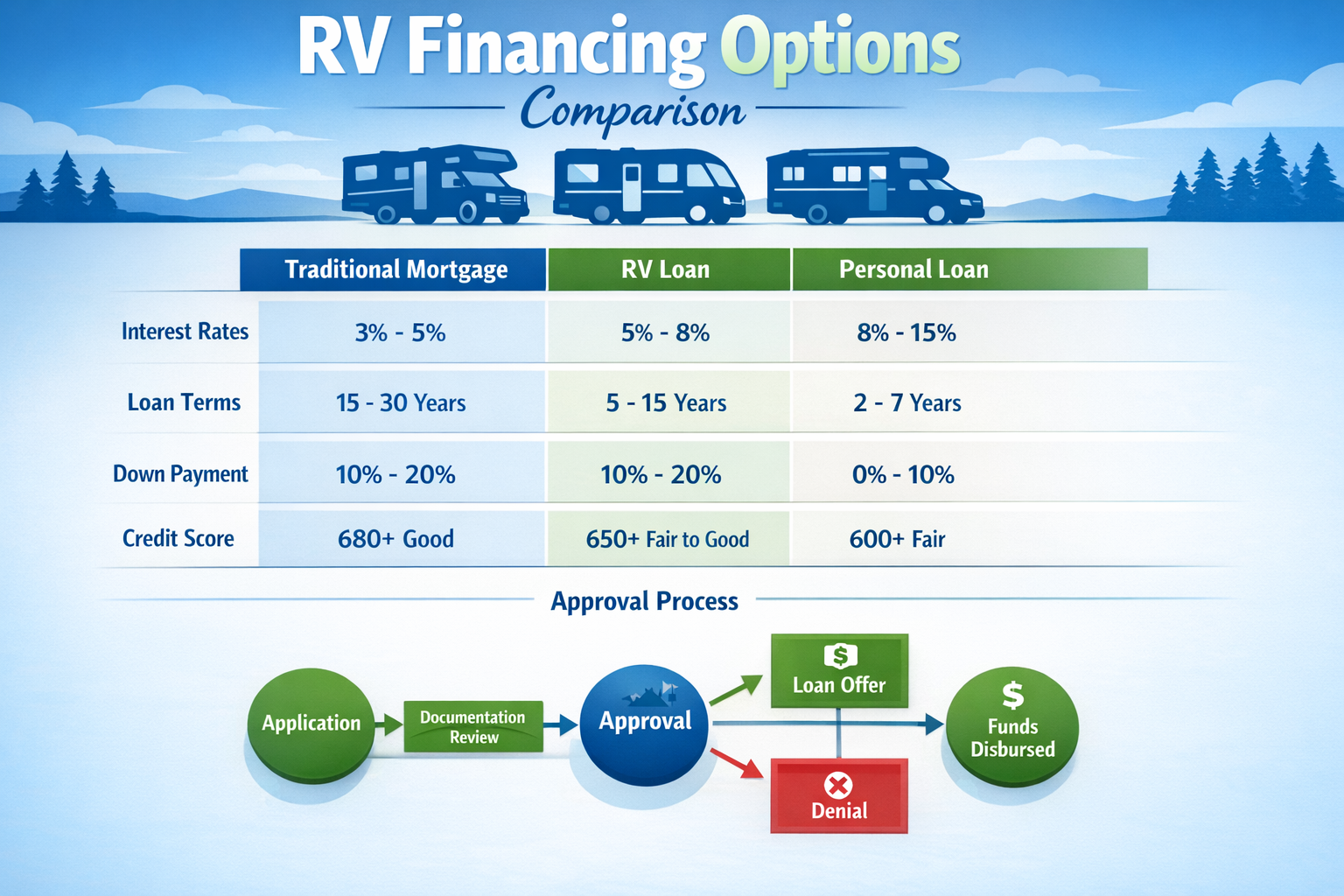

The short answer is: not exactly like a traditional mortgage, but yes, you can finance an RV. While the term “mortgage” typically refers to real estate loans secured by immovable property, RVs fall into a different category entirely. They’re considered vehicles or personal property, which means the financing landscape looks quite different.

Traditional mortgages are secured by real estate that appreciates over time, offering lenders substantial collateral. RVs, however, are depreciating assets similar to cars or boats. This fundamental difference shapes every aspect of RV financing, from interest rates to loan terms.

Why RV Financing Differs from Home Mortgages

When people ask “can you get a mortgage on an RV,” they’re often thinking about the 30-year terms and low interest rates associated with home loans. Unfortunately, RV financing typically involves:

- Shorter loan terms (usually 10-20 years maximum)

- Higher interest rates compared to mortgages

- Larger down payment requirements (often 10-20%)

- Stricter credit requirements for favorable terms

Types of RV Financing: Exploring Your Options Beyond Traditional Mortgages

Specialized RV Loans

RV loans represent the most common financing method for recreational vehicles. These loans are specifically designed for RV purchases and offer several advantages:

✅ Pros:

- Competitive interest rates for qualified buyers

- Longer repayment terms than personal loans

- Lower down payment requirements than some alternatives

- Specialized lenders understand RV values

❌ Cons:

- Higher rates than traditional mortgages

- The RV serves as collateral (risk of repossession)

- May require RV insurance throughout the loan term

Personal Loans for RV Purchases

For smaller RVs or those with excellent credit, personal loans can be an attractive option:

✅ Pros:

- No collateral required (unsecured)

- Faster approval process

- Flexible use of funds

❌ Cons:

- Higher interest rates

- Shorter repayment terms

- Lower loan amounts available

Home Equity Loans and HELOCs

If you own a home with substantial equity, you might leverage that equity for RV financing:

✅ Pros:

- Lower interest rates (similar to mortgage rates)

- Potential tax deductions (consult a tax professional)

- Larger loan amounts available

❌ Cons:

- Your home becomes collateral

- Risk of foreclosure if unable to repay

- May require home appraisal

Qualification Requirements: What Lenders Look for When You Ask “Can You Get a Mortgage on an RV?”

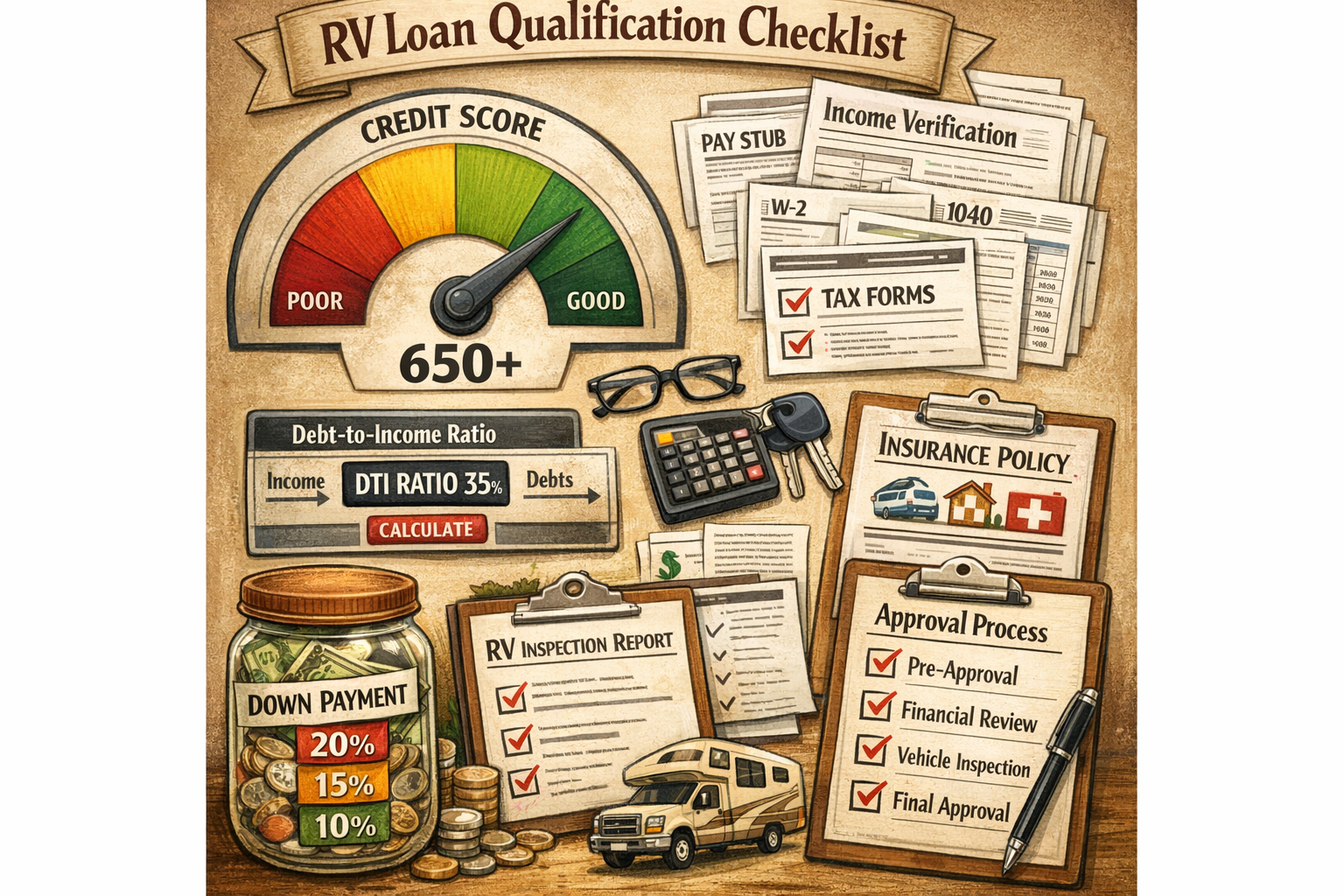

Credit Score Requirements

Your credit score plays a pivotal role in RV financing approval and terms:

| Credit Score Range | Typical Interest Rate | Approval Likelihood |

|---|---|---|

| 740+ (Excellent) | 4.5% – 6.5% | Very High |

| 670-739 (Good) | 6.5% – 8.5% | High |

| 580-669 (Fair) | 8.5% – 12% | Moderate |

| Below 580 (Poor) | 12%+ or Declined | Low |

Income and Debt-to-Income Ratio

Lenders typically require:

- Stable employment history (2+ years preferred)

- Debt-to-income ratio below 40% (including the new RV payment)

- Proof of income through pay stubs, tax returns, or bank statements

Down Payment Considerations

Most RV lenders require:

- 10-20% down payment for new RVs

- 15-25% down payment for used RVs

- Higher down payments may secure better interest rates

New vs. Used RV Financing: How Age Affects Your Mortgage Options

Financing New RVs

New RV financing typically offers the most favorable terms:

- Lower interest rates (often 1-2% less than used)

- Longer loan terms available (up to 20 years)

- Lower down payment requirements

- Manufacturer incentives may be available

Used RV Financing Challenges

Used RV financing comes with additional considerations:

- Age restrictions (many lenders won’t finance RVs over 10-15 years old)

- Higher interest rates due to depreciation concerns

- Shorter loan terms (typically 10-15 years maximum)

- Required inspections to verify condition and value

💡 Pro Tip: RVs older than 10 years may require personal loans instead of traditional RV financing, significantly impacting your monthly payment and total interest paid.

Interest Rates and Terms: The Real Cost of RV Financing

Current RV Loan Rates in 2026

RV loan interest rates in 2026 typically range from 4.5% to 12%, depending on:

- Credit score and financial history

- Loan amount and term length

- RV age, type, and condition

- Down payment percentage

- Lender type (banks, credit unions, or specialized RV lenders)

Loan Term Options

Common RV loan terms:

- 5-10 years: Higher monthly payments, less total interest

- 10-15 years: Balanced approach for most buyers

- 15-20 years: Lower monthly payments, more total interest

- 20+ years: Rare, typically only for luxury coaches over $200,000

Alternative Financing Options When Traditional RV Mortgages Aren’t Available

Dealer Financing

Many RV dealerships offer in-house financing or work with multiple lenders:

✅ Advantages:

- Convenient one-stop shopping

- Potential manufacturer incentives

- May work with various credit levels

❌ Disadvantages:

- May not offer the best rates

- Limited negotiation power

- Pressure to purchase additional products

Credit Union Loans

Credit unions often provide competitive RV financing:

- Lower interest rates than traditional banks

- More flexible qualification requirements

- Personalized service and local decision-making

- Member benefits and loyalty programs

Peer-to-Peer Lending

P2P lending platforms can be viable for smaller RV purchases:

- Flexible terms and qualification criteria

- Competitive rates for qualified borrowers

- Faster approval process

- No collateral requirements (unsecured loans)

Tips for Securing the Best RV Financing Deal

Shop Around and Compare Offers

Never accept the first financing offer you receive. Compare:

- Interest rates and APR

- Loan terms and monthly payments

- Down payment requirements

- Fees and closing costs

- Prepayment penalties

Improve Your Credit Before Applying

Boost your credit score by:

- Paying down existing debt

- Making all payments on time

- Avoiding new credit applications

- Checking credit reports for errors

- Keeping credit utilization low

Consider Timing Your Purchase

Strategic timing can save thousands:

- End of model years for better deals

- Off-season purchases (fall/winter)

- RV show events with special financing

- Manufacturer incentive periods

Negotiate Beyond the Interest Rate

Don’t focus solely on interest rates. Negotiate:

- Total loan amount and fees

- Down payment requirements

- Loan term flexibility

- Prepayment options

- Insurance requirements

Common Mistakes to Avoid When Seeking RV Financing

Overlooking Total Cost of Ownership

Many buyers focus only on the monthly payment while ignoring:

- Insurance costs (often $1,000-$3,000 annually)

- Maintenance and repairs

- Storage fees when not in use

- Registration and licensing

- Fuel and travel expenses

Borrowing More Than Necessary

Avoid the temptation to:

- Finance the maximum approved amount

- Add unnecessary accessories to the loan

- Extend loan terms beyond what’s comfortable

- Skip the down payment when possible

Not Reading the Fine Print

Carefully review all loan documents for:

- Prepayment penalties

- Variable rate clauses

- Insurance requirements

- Default consequences

- Hidden fees and charges

The Future of RV Financing: Trends and Predictions for 2026 and Beyond

Digital Lending Platforms

Technology is revolutionizing RV financing with:

- Instant pre-approval processes

- AI-powered risk assessment

- Streamlined documentation

- Mobile-first applications

Flexible Financing Models

Emerging financing options include:

- Subscription-based RV access

- Fractional ownership programs

- Rent-to-own arrangements

- Peer-to-peer RV sharing with financing components

Environmental Considerations

Green financing incentives for:

- Electric and hybrid RVs

- Solar-powered accessories

- Energy-efficient upgrades

- Sustainable travel practices

Conclusion: Your Path to RV Financing Success

While you can’t get a traditional mortgage on an RV, numerous financing options exist to make your dream of RV ownership a reality. The key is understanding that RV financing operates differently from home mortgages, with shorter terms, higher rates, and unique qualification requirements.

Your next steps should include:

- Check your credit score and work to improve it if necessary

- Calculate your total budget including ownership costs beyond the purchase price

- Shop around with multiple lenders including banks, credit unions, and specialized RV lenders

- Get pre-approved before shopping to understand your realistic price range

- Consider the total cost of different loan terms, not just the monthly payment

Remember that the best RV financing isn’t always the lowest monthly payment – it’s the option that fits your overall financial picture while allowing you to enjoy the RV lifestyle safely and sustainably. Take time to research, compare options, and choose financing that supports your long-term financial health.

Whether you’re dreaming of weekend getaways or full-time RV living, the right financing can turn that dream into reality. Start your research today, and you’ll be well on your way to hitting the road in your perfect RV! 🚐✨

{kind=link}