Dreaming of hitting the open road in your own motorhome or travel trailer? Before you start planning your first campsite, there’s one big question to answer: can you use an auto loan for an RV? The short answer might surprise you — and understanding the difference between loan types could save you thousands of dollars. 🚐💨

Whether you’re eyeing a cozy Class B camper van or a luxurious fifth wheel, financing your RV the right way matters. This guide breaks down everything you need to know about auto loans, RV loans, and the smartest way to fund your next adventure.

Key Takeaways 🗝️

- Auto loans and RV loans are structurally different — most lenders won’t approve a standard auto loan for an RV purchase.

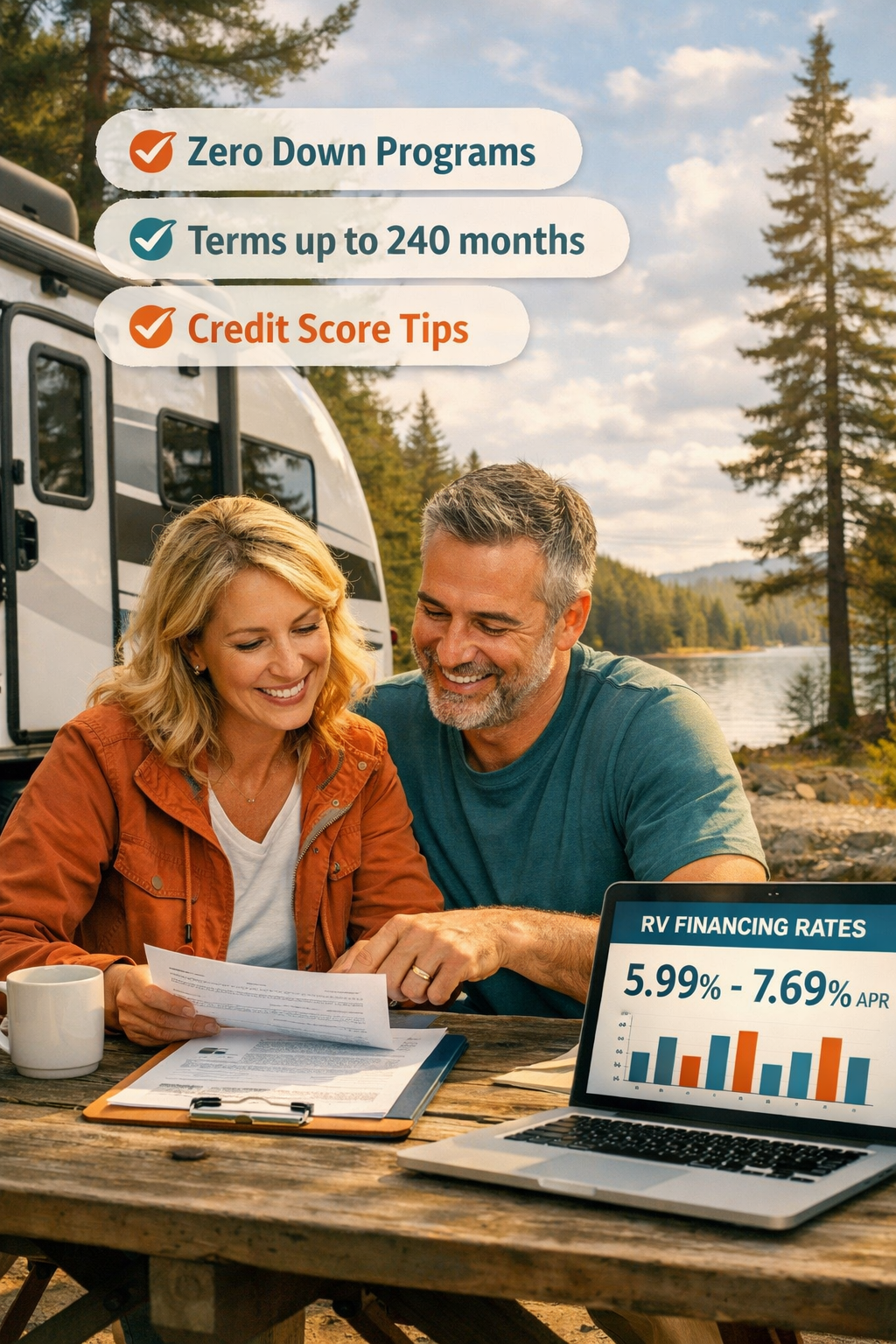

- RV loans offer much longer terms (up to 240 months) and loan amounts up to $1 million or more.

- Current RV loan rates range from 5.99% to 7.69% APR in 2026, depending on your credit profile.

- Personal loans are a backup option if your RV doesn’t qualify for a dedicated RV loan.

- Interest on secured RV loans may be tax-deductible if the RV qualifies as a second home — but the new IRS auto loan interest deduction does NOT apply to RVs.

Would you like to save this article?

Can You Use an Auto Loan for an RV? Understanding the Key Differences

This is the million-dollar question (sometimes literally). Technically, a lender could approve an auto loan for a small camper or towable trailer — but in practice, most traditional auto loans are not designed for RV purchases, and many lenders won’t allow it.

Here’s why:

Auto Loans vs. RV Loans: A Side-by-Side Look

| Feature | Auto Loan | RV Loan |

|---|---|---|

| Typical loan term | 24–84 months | 60–240 months |

| Loan amounts | Up to ~$100,000 | $5,000–$1M+ |

| Interest rates | Varies by credit | 5.99%–7.69% APR [2] |

| Collateral | Vehicle | RV (secured) or none (unsecured) |

| Tax deductibility | New IRS deduction (cars only) [6] | Possible if secured as second home [5] |

| Specialized features | Standard | Zero-down, noncitizen financing [2] |

RV loans are specifically designed for recreational vehicles like motorhomes, travel trailers, and fifth wheels. They come with different terms, rates, and eligibility requirements compared to standard auto loans [4]. Because RVs are more expensive and depreciate differently than cars, lenders treat them as a separate financing category entirely.

💬 “RV loans often include features like zero-down programs for loans up to $100,000 and same-day credit decisions — flexibility that standard auto loans simply don’t offer.”

Why Lenders Draw the Line

Most banks and credit unions categorize RVs differently from passenger vehicles. A Class A motorhome can cost $300,000 or more — far beyond the typical auto loan ceiling. Even smaller travel trailers often exceed what auto loan programs are built to handle.

Additionally, auto loan terms are much shorter — usually capped at 84 months. For a $150,000 RV, that means sky-high monthly payments. RV loans stretch repayment out to 10, 15, or even 20 years, making monthly costs far more manageable [4].

The Three Main RV Financing Options

When asking can you use an auto loan for an RV, it helps to understand what financing options actually exist [4]:

- Secured RV Loan — The RV serves as collateral. This typically means lower interest rates and better terms. Most common choice. ✅

- Unsecured Personal Loan — No collateral required, but rates are usually higher. Best for older RVs or smaller amounts.

- RV-Specific Loan Programs — Offered by specialized lenders with flexible features like zero-down options and noncitizen financing [2].

What to Know Before Applying for RV Financing in 2026

Now that the core question — can you use an auto loan for an RV — has been answered, let’s dig into what actually makes RV loans tick and how to get the best deal possible. 🏕️

Current RV Loan Rates and Terms

As of 2026, here’s what borrowers can expect:

- New RV loans: Average APR of 7.53% [2]

- Used RV loans: Average APR of 7.69% [2]

- Starting rates: As low as 5.99% APR for qualified borrowers [2]

- Loan terms: 60 to 240 months (5 to 20 years) [2]

- Loan amounts: Starting at $5,000–$10,000, with select lenders offering $1 million or more [2]

Your credit score plays a big role. Most lenders require a minimum score of 550–600, though the best rates go to borrowers with good to excellent credit [2].

Credit Score Impact on RV Loan Rates

| Credit Score Range | Likely Rate Outcome |

|---|---|

| 750+ (Excellent) | Best rates, ~5.99% APR |

| 700–749 (Good) | Competitive rates |

| 650–699 (Fair) | Moderate rates |

| 600–649 (Poor) | Higher rates, limited options |

| Below 600 | May need personal loan alternative |

What If Your RV Doesn’t Qualify?

Some older or high-mileage RVs don’t meet lender requirements for a dedicated RV loan. In that case, a personal loan is a solid backup option [2]. Personal loans don’t require the RV as collateral, so age and mileage restrictions don’t apply. The trade-off? Interest rates are typically higher, and terms may be shorter.

Tax Deductions: Auto Loan Rules Don’t Apply to RVs ⚠️

This is a crucial distinction for 2026. The IRS recently released guidance on a new auto loan interest deduction under the One Big Beautiful Bill — but this deduction applies only to qualified passenger vehicles for personal use, not to RVs [6].

So, can you still deduct RV loan interest? Possibly — but through a different route:

- Secured RV loans may allow interest deductions if the RV qualifies as a second home (it must have sleeping, cooking, and toilet facilities) [5].

- Unsecured personal loans used to buy an RV result in non-deductible personal interest [5].

- If combining RV loan interest with a home mortgage deduction, total qualifying debt cannot exceed $750,000 ($375,000 if married filing separately) [5].

💡 Pro Tip: Always consult a tax professional before claiming RV interest deductions. Rules vary based on how the loan is structured and how the RV is used.

Tips for Getting the Best RV Loan 🎯

- Check your credit score first — Even a small improvement can unlock better rates.

- Shop multiple lenders — Banks, credit unions, and online lenders all offer RV financing with different terms.

- Consider a larger down payment — Reduces the loan amount and may improve your rate.

- Look for zero-down programs — Available for loans up to $100,000 through select lenders [2].

- Compare secured vs. unsecured options — Secured loans usually win on rate, but unsecured loans offer flexibility for older units.

- Ask about same-day decisions — Many RV lenders now offer fast approvals, so you don’t lose a deal while waiting [2].

Conclusion: Skip the Auto Loan and Finance Your RV the Right Way 🚐✅

So, can you use an auto loan for an RV? While it’s technically possible in rare cases, it’s almost never the best move. Auto loans are built for cars — not for the unique size, cost, and lifespan of recreational vehicles.

RV loans are the smarter choice for most buyers. They offer longer repayment terms (up to 20 years), higher loan amounts, competitive rates starting at 5.99% APR, and specialized features that standard auto loans simply can’t match [2][4]. And if your RV doesn’t qualify for a dedicated loan, a personal loan gives you a solid fallback.

Your Action Plan 📋

- Check your credit score at a free service before applying.

- Get pre-qualified with at least 2–3 RV lenders to compare offers.

- Decide between secured and unsecured based on your RV’s age and your financial goals.

- Talk to a tax advisor about whether your RV loan interest qualifies for deductions.

- Start your adventure — the open road is waiting! 🌄

References

[1] Irs Releases Proposed Regulations For No Tax On Car Loan Interest Provision Under The Obbba – https://www.westerncpe.com/taxbyte/irs-releases-proposed-regulations-for-no-tax-on-car-loan-interest-provision-under-the-obbba/

[2] lendingtree – https://www.lendingtree.com/auto/rv/

[3] New Irs Auto Loan Rules Effective January 31 2026 Vehicle Qualification Interest Reporting Details – https://www.wisbank.com/events/new-irs-auto-loan-rules-effective-january-31-2026-vehicle-qualification-interest-reporting-details/

[4] Rv Loans For 2026 What To Know Before You Buy – https://mmccu.com/rv-loans-for-2026-what-to-know-before-you-buy/

[5] Rv Tax Deduction 2026 Blackseries Guide – https://www.blackseries.net/blog/rv-tax-deduction-2026-blackseries-guide.html

[6] Treasury Irs Provide Guidance On The New Deduction For Car Loan Interest Under The One Big Beautiful Bill – https://www.irs.gov/newsroom/treasury-irs-provide-guidance-on-the-new-deduction-for-car-loan-interest-under-the-one-big-beautiful-bill

[9] How Long Are Rv Loans – https://www.consumeraffairs.com/finance/how-long-are-rv-loans.html

[10] Rv Loans – https://www.bankrate.com/loans/personal-loans/rv-loans/

{kind=link}